Third World Chutzpah retailer leasing strategy for a wired world

By Mark Borsuk Managing Director The Real Estate Transformation Group property strategies for the information agesm For Financial, Credit and Internal Audit Executives Conference National Retail Federation September 22, 1997 San Diego, CA Copyright 1997 © Mark Borsuk. All Rights Reserved. chutzpah (Yiddish) - audacity, gall, nerve

Outline I. Leasing strategies for a wired world. II. The impact of information technology on shopping. A. How does information technology impact society? III. Online shopping's impact on store sales. A. Online shopping is just another sales channel. 1. Catalog's history. a. Community. G. Other online shopping impediments. 1. Credit card security. H. Other online services benefiting shopping. 1. Bill Presentment. I. The Year 2000 Outbreak. IV. Online shopping's impact on store economics. A. Does online shopping cannibalize store sales? V. Competitive pressures to enter cyberspace. A. Role of space. 1. Corporate downsizing. B. New Competitors. 1. Stealth Competitors. C. Wall Street sees value in online shopping. 1. Cybersurgeons. VI. Leasing strategy for a wired world. A. Changing the retail business model. 1. Metaphors and Mindsets. B. Reformat the leasing cycle to coincide with the tipping point. 1. Using Battle Management software. E. "If you don't ask for it, you won't get it!" 1. Rent. a. Fixed Rent. 2. Use. Graph & Charts

THIRD WAVE CHUTZPAH (1) retailer leasing strategy for a wired world By Mark Borsuk (2) I. Leasing strategies for a wired world. Online shopping's impact on retail store profitability is an over-the-horizon issue. Today most believe it will take five to ten years to develop a mass market for online shopping. There is little belief online shopping could cannibalize store sales and profitability. It is axiomatic that people change habits slowly, especially geocentric shopping patterns. However, what if common wisdom was more cliché than reality? What if underlying factors are predisposing consumers to purchase goods and services online? The implications for store profitability are staggering, and by implication so are prospects for space. The velocity of users joining the Internet portends an active online sales channel in three to five years. This is an issue presently confronting retailers. An over-the-horizon issue is how online shopping impacts leasing. While three to five years seems like a long time, in real estate it is the short term. Real estate commitments made today without planning for the development of an online sales channel could result in many unintended consequences. In several years, a third of US households will be online. These consumers are

attractive for retailers because of their income and educational levels. Buying online

will no longer be novel but a necessity for many people. Smart retailers will quickly

become online players, others will make the shift to stay competitive. One consequence of

increased online shopping is to pull sales out of stores and thereby make them less

profitable. Future leases must be flexible enough to accommodate early termination or

downsizing to support the addition of the online sales channel. Moving towards a wired

world requires retailers to consider the over-the-horizon issue of changing space use.

Planning for the transition will avoid later anguish.

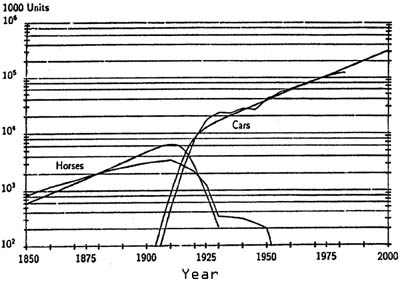

II. The impact of information technology on shopping. A. How does information technology impact society? Radio provides an example of how information technology changes a society (3). Military applications were one of the early ideas for using radio. Likewise the military designed the Internet to withstand a nuclear attack on the communication infrastructure. The early enthusiasts for radio were hobbyists. Likewise, the early users of the Internet were academics and computer enthusiasts. The standardization of parts and protocols created the 1920s' "radio mania." This led to the development of a national market for consumer products, along with homogenizing the culture and world view. By the 1980's the online world was developing and became a mass market in the mid-1990s. Email addresses and Web pages represent a new form of social status. Communicating with people worldwide and having previously unimaginable information readily available are creating expectations about what can be done in a wired world. Online shopping is one expectation. B. Technology's impact on existing practices and customs. The advent of the automobile is an example of technology displacing one form of activity with another. In less than fifteen years automobiles displaced horses as the primary means of transportation (4). Graph 1. While mechanical innovation transformed activities over years and decades, information technology can quickly displace existing practices. The Pony Express and silent movies are examples. The telegraph replaced the Pony Express in nineteen months (5) and the talkies decimated the silent movie industry within two years after commercialization (6). In each case there was a rapid and immediate acceptance of the transformation. Could the same be true for online shopping? How quickly could consumers adopt this form of information technology? C. Consumer acceptance of high-tech products and services is different.

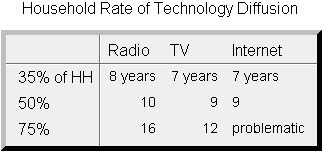

Unlike radio and TV, the Internet is a network. It is a one-to-one, one-to-many, many-to-one, or many-to-many information medium. Its intrinsic value to participants is apparent. Metcalfe's Law quantified the value. The law states the value of a network increases exponentially as the size of the network grows linearly. Telephones and faxes are excellent examples of how a simple increase in the number of users adds much greater value for the users (8). Currently, nineteen percent of households are online (9). Thirty-six percent will be online in 2000 (10). Put another way, it will probably

take seven years for the Internet to go from the early adopters to becoming a household

appliance. A June survey by Price Waterhouse found twenty-five percent of households with

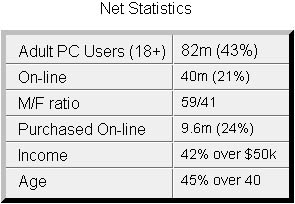

Internet access (11). The Business

Week survey below lists some important online user characteristics (12). Reaching a fifty percent penetration could parallel TV's diffusion. Almost all new PCs come with a modem and software for connecting to the Internet. Driving down the PC's price below $1,000 is also expected to expand the number of households (13). If services like WEB TV catch on, the diffusion could occur faster. In addition, the use of cable TV for Internet service is likely. Approximately sixty-five percent of households have cable (14). More consumers will seek the Internet access if they can do so without a computer. Services like WEB TV and the cable delivery systems being developed could greatly expand the number of households online (15). Penetration beyond fifty percent of households is problematic. A large segment of the population will not find the wired world compelling or useful. They are the Sidelined Citizens numbering seventy-one million (16). The same Price Waterhouse survey found thirty-five percent of participants said they would never get online. This is not surprising since many will remain satisfied to go shopping, contact others by phone instead of email, bank in person or by mail instead of online, and meet face to face instead of joining a virtual community. Thus, the impact of a wired world will be negligible for a number of retailers. D. Getting consumers to shop online. One technology forecaster believes examining certain consumer attitudes about high-tech product attributes provides important insight into how consumers will accept the new technology. Once accepted, their growth is exponential. Her analysis examines three variables: familiarity, gain and resistance (17).

The decision matrix illustrates the interplay among these attitudes for two familiar high-tech items and speculates on how online shopping fits into the schema. High-Tech Consumer Adoption Decision Matrix

It was clear at the outset consumers were unfamiliar with what programming meant and how to do it (Familiarity). Most did not see sufficient value in learning (Gain) and it became folklore that no one else could program their VCR (Resistance). Conversely, most people already knew how to use a phone and copy machine (Familiarity), saw the immediate benefit (Gain), and found little to complain about, especially as prices were falling (Resistance). It is interesting to note that the rapid decline in VCR prices had little impact on peoples' interest in programming. The decision matrix makes clear much more needs doing to meet the consumers' expectations and concerns. If online shopping is to become a natural shopping choice, retailers must provide a wide selection, have useful information, make the browsing and purchasing simple and convenient, and offer unbeatable prices that includes shipping. Finally, the automobile's history may offer a guide to gaining the consumers' allegiance. Early in the century cars lacked automatic starters and transmissions and required constant care. Over time many refinements made vehicles problem free and dependable. Similarly, retail sites have to strive to give a positive experience. III. Online shopping's impact on store sales. A. Online shopping is just another sales channel.

Conceptually, whether a consumer purchases a product or service in the store, from the paper catalog, or online, it is still a sale; only the venue changes. There are numerous examples where the point-of-sale changed or the sales channel reformatted. Milk and diary products were formerly delivered by a milkman. The advent of the supermarket made this channel redundant. Many stores used to have sales people on the floor to assist customers, yet most moved to a self-service format making the cashier the point-of-sale. Finally, as the population shifted to the suburbs, the downtown flagship store played a diminished role. B. Who does online shopping work for? On the maintenance-leisure continuum, maintenance/restocking shopping is more inconvenient than pleasurable. This sets the stage for a reaction against the "automobile as human prosthesis" life style characteristic for most people. Reducing travel time by shopping online would fulfill one important goal for them. This stands the store location mantra on its head. In other words, the premium location on the interstate becomes less convenient than buying online. The perceived lack of time may be attributable to the growing integration of work and leisure into a "seamless web" with all the attendant problems and conflicts, like taking a laptop on vacation or relying on day care (18). Interestingly, women feel more stressed than men and stress rises with income and education (19). The availability of useful shopping sites online could rapidly accelerate the diffusion of online shopping into the home, especially for higher income and educated consumers. Their migration online presents an attractive incentive for traditional retailers to get online. Also consider "me-time." Me-time represents the time-stressed individual's

effort to buy back time taken up by unfulfilling activities like non-recreational

shopping. Those seeking more "me-time" may very well pay a premium to receive

goods and services delivered to the home [groceries-www.peapod.com]

or prepaid by ordering online [movie

tickets-www.moviefinder.com]. C. Acclimating the consumer to an online presence. D. Shopping reflects available technology. E. What works online? Another way to look at what works online is to consider self-service shopping. The absence of a sales person to offer guidance and opinion covers a broad spectrum of goods and services. Self-selection also suggests that many things sold in self-service stores could work online. Goldman Sachs developed an "Internet Retail Index" to rank merchandise categories for their online sales potential (20). Categories with the highest potential were books, music, software, prescription drugs, computers, electronics and office products. Those considered to have the least current potential for migrating online were home furnishings, specialty apparel, auto parts, department stores, off price apparel, variety discounters and perishable food. The Goldman Sachs taxonomy parallels the continuum analysis and the author's tenant screen (21) with one important exception: apparel. If apparel works in catalogs it will work online. In 1996, three of the ten largest catalogers ranked by sales sold apparel: J.C. Penney, Spiegel and Land's End (22). F. Why is online shopping different from catalog shopping? Experience suggests on-line shopping will not affect store sales just as catalog

shopping did not appreciably impact store sales. The historical record supports this view

but history will be a faulty guide in the networked economy: the economy of the

Information Age. 1. Catalog's history. The Direct Marketing Association, a trade group, estimates catalog orders are about 4% of total consumer sales. There is very little evidence that catalog shopping cannibalized store sales (23). Rather, anecdotal evidence suggests the reverse: catalog sales help target future locations. However, when examining whether online shopping has a propensity to cannibalize store sales, each retailer's product category and customer profile requires assessment. It is misleading to analyze aggregate numbers. Retailers should also review the Morgan Stanley research report. The study suggests the growth of mail order is a reasonable proxy for the growth of online shopping volume. In discussing the impact of innovative retail concepts (category killers, catalogs, and home/TV shopping), the analysts can't decide whether it will or will not have an impact on how retailers do business, i.e., store based retailing (24). But they suggest Internet retailing could grow 3-5 times faster than mail-order (25). 2. The different worlds of catalog and online shopping. There are three attributes that set online shopping apart from catalog shopping. These attributes create a fundamentally different experience for shoppers in ways not possible in the store or from a paper catalog. a. Community. Community is the first attribute that distinguishes the online world from catalogs. Retailers need to familiarize themselves with the virtual community concept popularized in net gain (26). Net gain is a blueprint for the commercial online business model. In essence, community means adding value for the customers who become active participants. The virtual community concept is rapidly gaining support among academics, analysts, consultants and practitioners (27). Amazon.com [http://www.amazon.com] is an example of a virtual community. Amazon.com creates a community by soliciting book reviews from customers and through "Eyes" notifies them when new titles of special interest arrive. In other words, the customers play an active part in the development and expansion of the site. This attracts others and increases the value of the site. Barnes & Noble [http://www.barnesandnoble.com] estimates online book buyers may purchase 5-10 times as many books as regular customers (28). On the negative side virtual communities will likely reduce margins (29). Other examples of virtual communities are PikeNet [http://www.pike.net] and Auto-by-Tel [http://www.auto-by-tel.com]. PikeNet is not a retail site but a service site for the commercial real estate community. It offers marketing and analysis tools for commercial real estate brokers. The site naturally leads to networking and may ultimately become the precursor for a national multiple listing service. Auto-by-Tel offers automobile buyers pricing and product information, side-by-side comparisons, expert opinions, user input, links to other useful sites and feedback from purchasers. Why should the buyer go anywhere else to start looking? This is an example of how the community can provide immediate and useful information. Links to other useful Web sites strengthen the sense of community. For example, Amazon.com and Barnes & Noble pay a commission for becoming the exclusive book store on their partners' sites. It would be similar to a rock climbing club receiving a commission every time one of its members purchases a book from a specific book store. Another form of community service is L.L. Bean's link to National, State and local parks. The site contains significant information on each park along with L.L. Bean's clothing and accessory recommendations. The essence of community validates Metcalfe's Law. No paper catalog is able to create the positive feedback customers have when connected to an virtual community. b. Selection and product information content. The second attribute is selection and information content. Online book sellers like Amazon.com offer a selection of in-print books vastly larger than any Barnes & Noble superstore. Auto sites like Auto-by-Tel can provide more specifications and ancillary information than any dealer and side-by-side comparisons. Travelocity [http://www.travelocity.com] provides the lowest air fare quickly without human intervention, and tickets may be purchased online. These and hundreds of other sites give consumers the necessary information to make intelligent product comparisons and purchase decisions. In the physical world information is power and the online world shifts the power to the consumer. c. Custom marketing and customer service. The third attribute is custom marketing and customer service. Once a customer places an order or provides an email address, the retailer can anticipate the customer's requirements by analyzing her shopping pattern. Just remembering a customer's last purchase is a desirable feature. The merchant's site can alert the customer through email of new items likely to appeal to them, special discounts, promotions or order opportunities, and myriad of other suggestions likely to appeal to the customer. Customers can express their preferences in surveys, contests and discussion forums all done online. This becomes a valuable source of marketing data leading to product differentiation and value added. The paper catalog pales in comparison to the immediacy of the response and impact customized marketing can have on customers. In addition, handled properly, the interaction strengthens the customer's sense of community. The unique nature of online shopping demonstrates the danger of comparing the online world to the catalog experience. Rather, the evidence strongly suggests online shopping has the attributes for driving sales out of stores. Further, as traditional catalogers move online, consumers will begin to expect the same from retailers. In a perverse way, the traditional catalogers who had little impact on store sales may train their customers to shop outside the store. This would be an example of the law of unintended consequences at work. IV. Online shopping's impact on store economics. A. Does online shopping cannibalize store sales? Online shopping's special characteristics suggest, unlike catalogs, it will have an impact on store sales. However, even if online shopping develops as indicated, there would not be a wholesale shift in purchases away from stores. Rather the impact will be at the margin. Thus, the critical question to ask is what will be the marginal shift in sales? Were it to be between 8% and 12%, what will be the impact on store profitability? The CFO's challenge is to estimate the change in store profitability from each dollar of lost sales and how quickly profitability declines. The larger the marginal shift, the greater the incentive to implement the third sales channel in an effort to retain sales and align leasing strategy for a wired world. B. Push-Pull conundrum. How quickly online sales will grow and impact individual retailers is uncertain. What is certain is today a growing number of consumers are purchasing goods and services online. There is even a magazine for online shoppers [http://www.internet-shopper.com]. Over the next several years customers will pull retailers online, retailers will push consumers online or there will be a combination leading to a rapid growth in sales and merchants online. Retailers will need to consider whether their current customer base and selection will result in a migration to cyberspace. Leveraging the online channel may require new merchandise or going after new customers. Today, banks, stockbrokers, mutual funds, hotels, car rental agencies, airlines, membership organizations and of course Microsoft are teaching consumers how to shop online. Stock trading is an example of how quickly the Internet can propagate a good idea. Currently, there are approximately 3 million online trading accounts generating an average of 95,000 trades per day. The accounts could exceed 14 million by 2002 according to one estimate (45). Even movie tickets are available online! C. It's Technographics not Demographics. D. Locating consumers with a propensity to shop online. It is possible by analyzing telephone service areas to develop an estimate of the online population within a geographic area. The first three digits of the seven digit local phone number correspond to a service area. The estimate requires knowing the total number of modem connections (dial-up ports) for each Internet Service Provider (ISP) and the ratio of ports to users. The next step requires contacting the ISPs to learn the number of POPs (points of presence phone numbers) they maintain within each area code and the number of non-dedicated phone circuits assigned to each POP number. Analyzing the above information yields the potential number of online users within a defined area which retailers can use along with their traditional demographic data to plan sales channel strategy. For example, it could help them decide whether to open a new store, add another store within the same trade area or to downsize an exiting store into a different format. A portion of the information is publicly available in Boardwatch Magazine

[www.boardwatch.com]. Boardwatch lists ISPs nationwide by area code. There are over 4,000

ISPs in the US and Canada. Developing market intelligence about local concentrations of

online users is critical to reaching the estimated 41.9 million shoppers' online in 2001(46) and selecting the most profitable

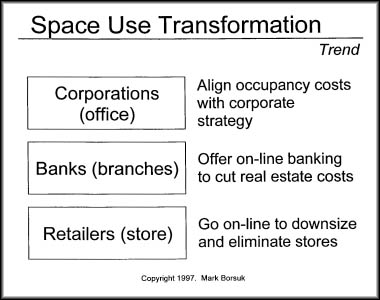

channel mix. V. Competitive pressures to enter cyberspace. A. Role of space. 1. Corporate downsizing. The Internet is one manifestation of the transition into the Information Age. A hallmark of the transformation is the changing nature of wealth. In the industrial age physical capital in the form of buildings and machines signified wealth. However, in the Information Age intellectual capital creates even more wealth. This means the people in the building are more valuable than the buildings themselves. One sign of this is the pursuit of core competencies and reengineering business processes to increase shareholder value (47). The emphasis on increasing shareholder value has had a profound impact on the role of real estate in organizations. Over the last decade, manufacturing and service firms aligned space demand with corporate strategic goals. Cost reduction and rationalization followed. Firms directly linked real estate to the business plan and developed financial metrics for evaluating how space influences return on investment. Corporations needed to analyze real estate's contribution to the firm's strategic goals. This recognition grew from the efforts of academics, industry groups, and management consultants to correctly price and manage occupancy costs (48). The results are favorable, and one large office user reported slashing occupancy costs by fifty percent (49). The senior management understood they could do with less space, that space costs had to align with corporate investment goals, and that all real estate decisions had to further shareholder value. 2. Branch banking. The Banks are going through the same space reduction process to achieve increased profitability made possible by technology. Traditional branch banking is being evaluated along with online banking and smaller units operating in supermarkets and other convenience locations. Many bank branches are redundant. In total they occupy more space, 250 million square feet, than general merchandise department stores (50). One analyst predicts, "Half of today's 60,000 branches will likely be gone by the end of the decade." (51) In addition, branch transaction costs cannot compare with online banking. A Booz-Allen & Hamilton survey found the cost of doing a transaction at a teller window is $1.08 but only $0.13 to do the same transaction over the Internet (52). No wonder banks are struggling to create incentives for moving customers online. Household online banking is rapidly increasing. In 1996, 2.5 million (3.1 %) of households banked online. By 2002, the number could reach 18 million (18.6%) (53). These are very compelling reasons for bankers to rethink their business model of branch banking to reduce real estate and overhead costs. 3. The third transformation in space use is retail. Retail CFOs can learn from the corporate and banking experiences and incorporate them into the development of the third sales channel. See Chart 1. There will be much resistance to the contemplated change. Few will readily accept the notion of merchandising and shopping online and its implications for leasing strategy, although a consulting firm analysis of online shopping done in 1994 noted cost savings from space reduction (54). Three years later what was intelligent speculation is starting to look more probable. 4. Retail consultants pushing change. Already, consulting firms are outlining how retailers will need to change their real

estate strategy (55). The corporate

experience and the trend in branch banking to generate greater shareholder value set an

important precedent. The June 1996 Deloitte & Touche study on electronic commerce found that a retailer who had superior locations and low cost leases would not have an advantage in a wired world (56). The importance of the observation was not only its implication but also its source. Ernst & Young expanded on their real estate theme in a survey releasedin June (57). The survey's breath was impressive. There were 252 respondents with average sales of $1.3 billion per year. They had an average of 230 locations containing 25,000 sq. ft. per location and 73% were leased. The three most important variables for siting store location were sales potential, population, and geographic location. Some of the findings were startling. Most respondents believed their current real estate plans were only good for two to five years but had thirteen year average lease terms. Nearly a third of the retailers lacked an overall real estate strategy. Finally, there was a significant gap between corporate strategy and real estate practices. In a wired world retailers cannot afford negative arbitrage by making long-term real

estate commitments while executing short-term strategies. Retailers need to elevate real

estate planning to a core competency similar to merchandising and supply chain management.

Store leasing should be flexible enough to accommodate format obsolescence, shorter

tenancy, exit strategies and plans for reuse of redundant space. Increasing shareholder

value dictates such action. B. New Competitors. The INFOTECH revolution will create a new retail landscape and business model. An online presence offers retailers the opportunities to increase sales, reduce costs, and expand market share. They also face competitive pressures to move online. There will be direct competitors in cyberspace along with their traditional rivals, catalogers, and Microsoft (58) albeit indirectly. The most worrisome competitors for retailers are the stealth competitors. 1. Stealth Competitors. Stealth competitors are new phenomenon in retailing (59). See Chart 2. Retailers should fear these apparitions for they are only found in cyberspace. Stealth competitors appear without warning on the consumer's computer screen. Retailers who lack a presence online can be easily blindsided by them. Amazon.com is one of the most successful stealth competitors. It competes directly with Barnes & Noble, Crown Books, and Borders but has no physical presence. The lack of real estate, store employees, almost no inventory and other cost savings gives Amazon.com a tremendous competitive advantage. Morgan Stanley's report contains an important case study for retailers on the guerrilla war raging between Amazon.com and Barnes & Noble. Their struggle receives continual financial press coverage and is the cause celebre for online merchants. There are two types of stealth competitors. The conflict between Amazon.com and Barnes & Noble offers important lessons for retailers. Among them are that stealth competitors immediately begin lowering prices, which leads to a price cutting death spiral. Established retailers seeking to meet the new prices cause inconsistent pricing between their stores and Web sites . This can act to drive store customers online. Stealth competitors steal market share. First Movers capture mind share (attention) that may not be recaptured easily by the established merchant entering the online market. This means that retailers holding back on establishing a Web presence should seriously consider the disadvantages of not being first online. However, it gets worse. To date, stealth competitors have been undercapitalized raiders, relying on their wits and new technology to challenge established, well capitalized retailers They are the Stealth-A competitors. However, there is reason to believe others can as easily enter the market. Established retailers like Wal-Mart [http://www.wal-mart.com] can quickly enter a new market leveraging their brand equity, technological skills and merchandising prowess to become a formidable new competitor overnight. They are the Stealth-B competitors. Stealth A and B competitors present a serious threat to retailers. They must ask themselves how quickly others online will begin diverting sales away from their stores. C. Wall Street sees value in online shopping. In 1997 Wall Street began noticing online shopping. Four major firms issued reports between February and August. The market is focusing attention on how online shopping will impact retailers. Each analysis took a different approach in estimating the importance of online shopping to the future of retailing. The most significant real estate insight came from Robertson Stephens' analysts (60). The analysts confronted the cannibalization issue directly. They said, "We believe that traditional retailers need to acknowledge the opportunity and/or threat of e-tailing. This is particularly true given that even a small percentage decline in same store sales levels can destroy the profitability of a retail store." (61) Bear Stearns had already demonstrated how cannibalization would cause a planned Borders Superstore to perform poorly due do to online competition (62). Morgan Stanley issued a comprehensive report covering a number of interrelated issues relevant to retailers (63). Goldman Sachs went on to develop an index to reckon the migration potential of goods and service into cyberspace (64). Bear Stearns had already looked at the impact on selected retailers (65). Wall Street's fascination with online shopping should concern traditional retailers.

Analysts' comments and writings send important signals to the investor and lender

communities about companies, their strategies, and prospects in a wired world. Goldman

Sachs noted, "Store-based retailers should go on-line and aggressively challenge

upstart competitors if the category is well suited for the Net, but they must realize that

in doing so, they are contributing to the creation of a permanent challenge to their

existing store base." (66)

Last July Barrons' carried an important article about the growth of online commerce. The

article noted the prospects for online shopping were good and growing for a variety of

retailers. This is another indication of the market expecting an aggressive push into

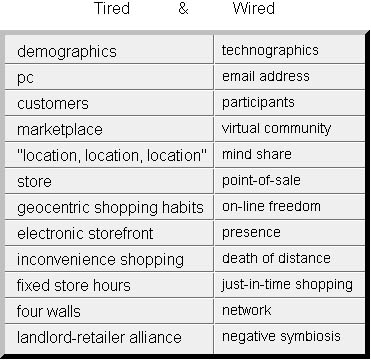

online retailing (67). 1. Cybersurgeons. Not only do retailers have to contend with their traditional rivals and emerging stealth adversaries, but with the possibility of a new kind of corporate raider stalking them: the Cybersurgeon. Cybersurgeons are corporate raiders transmogrified, who understand how to use INFOTECH and the leverage inherent in the emerging online sales channel to boost shareholder value. Retailers slow to implement change will be their prey. The Cybersurgeons will appear when market leaders like Wal-Mart demonstrate the channel's viability. Online retailing could very well change the financial performance of stores by marginally shifting sales to cyberspace. The impact of online shopping would vary by product category and retailer's unique customer base. There is growing recognition online shopping can challenge the geocentric shopping model and undermine current real estate strategy. External pressure from stealth competitors, Wall Street analysts and cybersurgeons require retailers to understand the coming structural change, plan for change and develop an online presence commensurate with its merchandising strengths and customer proclivities. One critical component of change will be to develop a leasing strategy for a wired world. VI. Leasing strategy for a wired world. A. Changing the retail business model. 1. Metaphors and Mindsets. If consumers are shopping and the retailers have a presence online, then what will be the impact on stores locations, formats and leasing strategy? The advent of online shopping requires retailers to rethink their business model to incorporate the interplay between the physical and the incorporeal. It requires a new mindset and set of metaphors. 2. Metaphors make a difference. The mental image of a store distorts one's ability to analyze the structural shift ahead. In other words, our metaphors imprison our thinking. See the following table. Like the landlord, the merchant's metaphors evoke rich images of shapes and textures related to physical space. However, to fathom cyberspace's impact, new metaphors are necessary to affect decisions and how they are made. Many retailing metaphors are related to infrastructure. Infrastructure means the emotional investment in the present business model, legacy systems, existing management, and stores (68).

In essence, INFOTECH makes presence as important as place. Several examples illustrate how physical location metaphors circumscribe the possibilities of the immaterial environment. Mind share, not location, signifies having the consumer's attention is every bit as important as having a terrific location. Point-of-sale, not store, captures the idea of sales migrating online. Participant, not customer, signifies the elevated status of the individual as they seek a richer experience online than is possible in a traditional venue. 3. Your success becomes your failure. A retailer with a successful location strategy faces a particular disadvantage. The

very metaphors, heuristics and experiences of the strategy make integrating a cyberspace

presence much more difficult. Their success is with the tangible while the intangible, the

antithesis, is the terra incognito. Thus, successful retailers will need to change their

mindset and undertake institutional change. B. Reformat the leasing cycle to coincide with the tipping point. In the year 2000 online shopping will take off. This requires retailers to develop a leasing strategy complementary with the channel's development. The strategy needs to build flexibility into new leases and to revise existing leases on renewal or earlier to gain channel flexibility. Goldman Sachs believes the Internet will have a meaningful to major impact on retailers in two to three years (69). Likewise Morgan Stanley sees a similar impact for selected retail categories (70). Planning should begin now to phase in early termination rights, space contraction and expansion rights, and other key changes in the economics for new leases or options to be exercised after 2000. C. From in-line to online. The advent of the cyberchannel will change how retailers site new stores, the number of stores within a trade area and store format. Additional new stores and their format will increasingly become linked to the local population's propensity to shop online by analyzing the number of online users within the trade area. This will also be true for maintaining existing stores and their formats. Existing store formats should undergo scrutiny to bring them into synchronization with

the customer base. In many instances, moving to a showroom format sans inventory will

provide retailers with a location for their non-wired constituency but save them part of

the cost for inventory space.

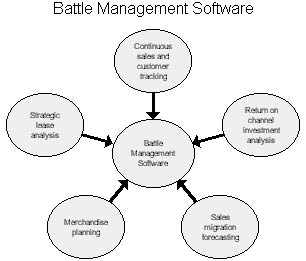

Battle management software illustrated above can provide continuous feedback and analysis to maximize channel value and allocate resources to maximize return. It should track the location of online shoppers and compare their zip code with the closest store to determine the extent of sales migration. The software would seek to discover opportunities from merchandising in each channel or combination of channels by use of financial metrics to uncover what works online versus what works in the store and/or the catalog. Another feature should be to aid leasing strategy based on sales migration patterns.

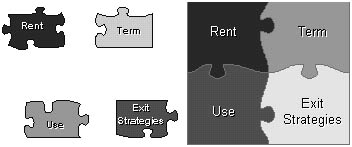

This would help align real estate leasing tactics with corporate strategic goals. E. "If you don't ask for it, you won't get it!" Flexibility is the key to leasing strategy in a wired world. However, flexibility for the tenant is at the expense of the landlord. Thus, retailers who embark on reformatting the sales channel will need to compensate landlords in some measure for the possibility of shorter terms or reduction in space. Lenders will also have to go through the same soul searching process. Ultimately, after the shouting dies down profit opportunities will dictate pragmatic solutions to these issues. The tenant's need for flexibility when properly structured can be reduced to a cost, e.g., liquidated damages, and measured against the anticipated gain from freeing resources in one channel for deployment to another. Inducing flexibility into the retail lease will not be easy. Today, few landlords can accept the networked economy's fundamental truth: INFOTECH severs place from activity and the concomitant shift in negotiating leverage to the tenant. Putting Metcalfe's Law in a real estate context also suggests why power is flowing to the tenant. This is because there is an inverse relationship between the value of the network, the Internet, and the value of the location, the store. That is, when activities move from physical space to cyberspace they enhance the value of the network and depress the value of location. While retailers should not expect to win many battles at this early stage, they must remain focused on developing an online sales channel and building flexibility into their leases. The illustration below presents the broad changes retailers must make in

leasing practices. They incorporate INFOTECH's dictates and reflect a number of

contemporary practices seen in a new light. These options are not free, but failing to pay

the price in the short term will multiply the cost many times in the long run. 1. Rent. a. Fixed Rent. INFOTECH promotes the disintermediation of space by reducing the location premium imputed in the rent. The rent commanded for space is likely to change and retailers should consider how they can bargain for cheaper rent or persuade landlords to allow them to convert the fixed rent obligation to a variable rent based on a percentage of the gross. Changing to a variable rent obligation would give retailers greater flexibility in managing their sales channel strategy. However, a fixed rent obligation is the sine qua non of the retail lease. It is almost impossible to contemplate a change in the short term. Nevertheless, INFOTECH's impact on space demand requires retailers to continually consider the issue in leasing strategy. b. Percentage Rent. There are several different concerns related to percentage for retailers (71). One would be not allowing the landlord to impute an unnatural breakpoint in sales thus increasing the rent as sales migrated online. Another is the Virtual Emporium [http://www.vemporium.com] problem. The Virtual Emporium is a retailer that allows customers to surf the Net and purchase selected goods and services online (72). In effect, it offers training wheels to the curious who lack access to the Internet and those who wish to learn how to shop online. One potential problem ahead for retailers would be if the Virtual Emporium were also a mall tenant and their customer ordered from the retailer's online site. Would the landlord contend the sale counted towards the tenant's percentage rent? Many similar questions will arise on this topic in the years ahead. 2. Use. 3. Term. The Ernst & Young survey highlights the mismatch between store longevity and lease term. One solution is to take a significantly shorter initial term with multiple short-term options. Obtaining a three to five year initial term with short-term options can be an optimal way to hedge the need for space and to maintain sales channel flexibility. 4. Exit Strategies. Early lease termination is not new in retail (73). Some retailers bargain for the right when they go to an uncertain market. The tactic takes on renewed vigor as the online sales channel gains prominence. Retailers should consider the full panoply of exit strategies to maintain sales channel flexibility. They can be based on minimum sales targets or be exerciseable after a certain number of years. It could be a one-time right, exerciseable at specific times, or an ongoing right. Several variations are possible. The kick-out right whereby the tenant ceases all operations based on the failure to meet a predetermined sales target. The go dark right whereby the tenant remains in possession but only pays occupancy costs, terminating all other operations. The tenant could also have the right to put the space back to the landlord for a predetermined payment. There are a wide variation of exit strategies and most retailers know how to bargain for them. Obtaining them is another matter. Nevertheless, the development of the online sales channel requires a number of exit strategies to be incorporated into the leasing strategy. The lease provision changes outlined above only begin to suggest the scope of change

ahead in the landlord-tenant relationship as retailers undertake sales channel

reformation. The rise of the networked economy diminishes the value of location for

landlords and retailers. It also dictates the need to change leasing practices. VII. What's ahead? Today, investing in the third sales channel represents a significant commitment of capital and human resources along with an uncertain outcome. Deferring the decision too long invites stealth competitors or worse, a hostile takeover by cybersurgeons. One important variable in developing the third sales channel is the best use of space. This challenges an organization's culture and mindset. Many retailers can proudly point to their premier locations as proof of their success. Even in a fully wired world, location based retailing will be the norm, but the number of stores, their location and size will undergo transformation. Retailers with chutzpah will create the leasing strategy necessary for enhancing shareholder value. 1. "Chutzpah is that quality enshrined in a man who, having killed his mother and father, throws himself on the mercy of the court because he is an orphan." Leo Rosten, The Joys of Yiddish, McGraw-Hill, New York, 1968. 2. The Real Estate Transformation Group advises property owners, tenants and lenders on

the impact of information technology on commercial property. In addition to consulting,

Mark Borsuk is a retail leasing broker and real property attorney. Mailing address: 1626

Vallejo Street, San Francisco, CA 94123-5116, (415) 922-4740, FAX 922-1485, mborsuk@ix.netcom.com.

Arnulf Grubler, Time for a Change, Rates of Diffusion of Ideas, Technologies, and Social Behaviors, WP-95-82, International Institute for Applied System Analysis, Laxenburg, Austria, 1995, p. 31.

Cybermalling-A Retail Death Sentence?, Journal of Property Management, Third Wave Wipeout: Do retailers need landlords in a wired world? The Challenge of Information Technology to Retail Property, Urban Land, February

1997. Will On-line Shopping Impact Retail Leasing? Technology complicates real estate investing, Pensions & Investments,

January 20, THIRD WAVE TSORIS: Do Real Estate Investment Fiduciaries and Appraisers Have THIRD WAVE WIPEOUT: INFOTECH’s Impact on Retail Space Demand. Third Wave Wipeout: Commercial Property Investment in the Information Age., Is Commercial Real Estate Investing Still Profitable in the Information Age?, What Is the Impact of INFOTECH On Commercial Real Estate?, SIOR Don’t be a Cyberputz, California Real Estate Journal, March, 1996. Real Estate Tax Policy for the Information Age, Real Estate Review, Commercial Real Estate: Road Kill On The Info Highway?, Microtimes, News Releases | Articles | Upcoming Talks | Memorable Quotes Copyright ©1995 - 2020. Mark Borsuk. All rights reserved. Disclaimer notice |